The Next Era of Private Credit

The Expanding Opportunity for Private Credit in U.S. Real Estate

RESEARCH

PGIM | $1.4T AUM

4/3/202510 min read

While uncertainty continues to challenge sentiment and activity, the stability and resilience of private real estate credit can provide a reliable income stream with built-in downside protection.

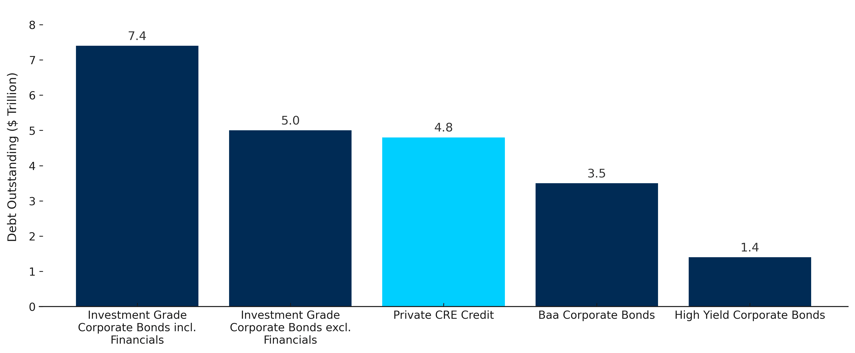

• At $4.8 trillion the U.S. private CRE credit market is an asset class comparable in size to major fixed income markets, offering a robust foundation for diversified investment.

• Private CRE credit enhances portfolio returns by providing predictable income streams and downside protection, while maintaining low correlation to other major asset classes, minimizing additional risk.

• Normalizing interest rates drive high current income while a recovering real estate market strengthens credit fundamentals, boosting the potential for solid returns on new investments while reducing risk.

• Increased need for debt capital, driven by loan maturities, building modernization needs and selective bank appetite, creates opportunities for alternative and flexible financing solutions.

• A growing range of property types, including operational assets, provides an expanded universe of investment opportunities, allowing for greater diversification and higher value-creation potential.

Executive Summary

A new private credit ecosystem is emerging across asset managers, banks, and insurers. Here’s what it means for the industry.

Why Private CRE Credit Makes Sense Now

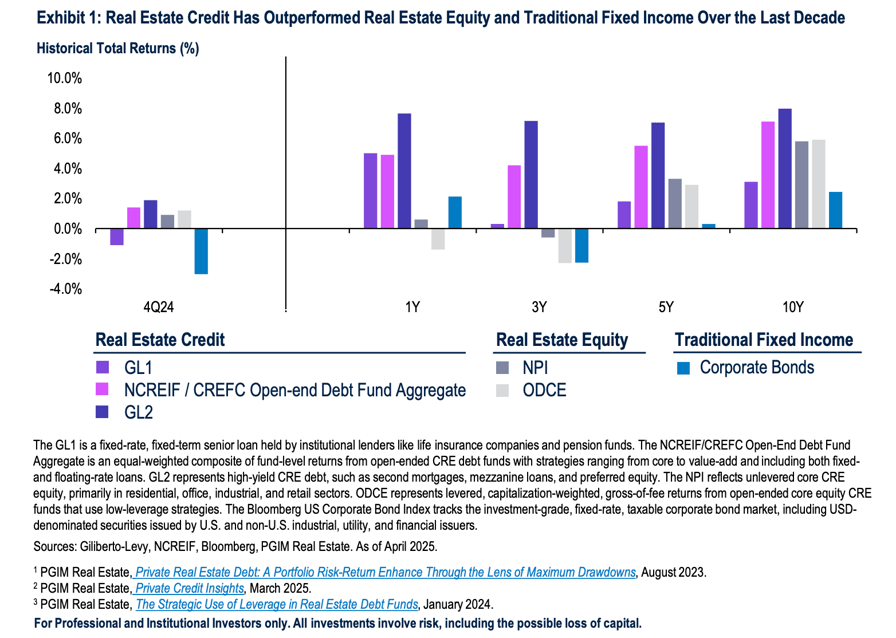

Private commercial real estate (CRE) credit has outpaced both real estate equity and traditional fixed income in total returns over the past decade, a period marked by a significant reset in property values.

While CRE credit has historically outperformed traditional fixed income, the recent downturn in real estate has contributed to its outperformance relative to equity (Exhibit 1). With risk-free rates now higher than in the previous cycle, real estate credit is expected to continue performing well.

With a focus on income-driven approaches offering downside protection and capital preservation, real estate credit provides a predictable income stream with lower volatility compared to real estate equity and traditional fixed income.

As the market continues to face uncertainty, we are reminded of the stability and resilience of private real estate credit, and the downside protection it brings.

Moreover, the current market environment, characterized by elevated but moderating interest rates, offers a solid income stream. Conservative attachment points also provide significant equity cushions, enhancing principal protection.

As the real estate market approaches recovery, a specific segment of the private real estate credit market warrants closer attention: financing for valueadd business plans. This strategy primarily utilizes floating rate loans, which mitigates interest rate risk, while strategic leverage can boost returns without adding property or credit risk. This segment benefits from increased demand for shorter-term loans as borrowers anticipate future rate cuts.

1) A $4.8 Trillion Asset Class

• The U.S. private CRE credit market, valued at $4.8 trillion,4 represents a substantial asset class on par with major fixed income markets (Exhibit 2).

• This depth allows for a diverse array of loan structures, with varying durations and secured by a broad range of property types across multiple locations. The diverse credit profiles of the underlying tenancy further enhance the market's diversification potential.

• Despite its private nature, the private CRE credit market offers significant breadth, providing investors with ample opportunities to strategically allocate capital to assets that align with their investment goals and risk profiles.

2) Portfolio Enhancing Features

• Private CRE credit has outperformed major fixed income asset classes while exhibiting lower volatility. This combination has delivered Sharpe ratios nearly twice those of other fixed income indices, positioning it as an attractive choice for optimizing portfolio risk-adjusted returns.

• With correlations of less than 100% to traditional fixed income investments, private CRE credit provides diversification benefits to fixed income portfolios.

• From a risk management standpoint, private CRE credit has exhibited less severe and shorter-lived maximum drawdowns compared to other fixed income assets, helping to limit portfolio losses during periods of financial market turmoil and drawdowns.

3) Improved Risk-Return Profile

• The rise in interest rates has benefited floating rate loans by increasing coupons, and thus, absolute returns on private CRE credit investments.

• Private CRE credit will continue to offer high current income, even as interest rates moderate.

• While elevated coupons may strain a borrower’s ability to pay interest, the expected recovery in the real estate market will enhance property cash flows, improving debt serviceability.

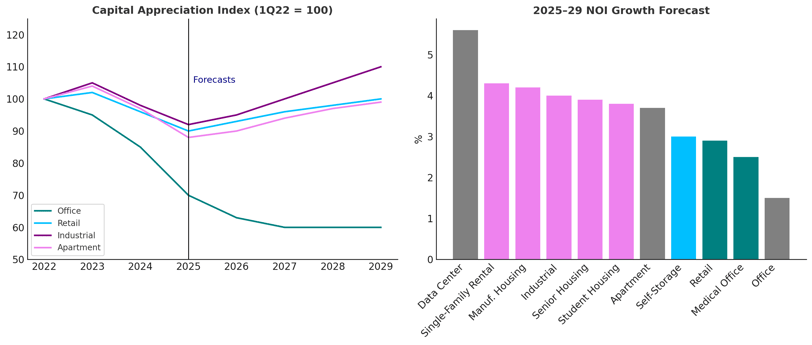

• Loans originated now are expected to experience declining credit risk over time as income and property values are forecast to grow (Exhibit 4).

• Higher income and stronger credit fundamentals together provide the potential for solid returns on new CRE credit investments.

4) Growing Need for Debt Capital

• Maturity Wall: High volume of maturities, due to loan modifications and extensions, drive demand for refinancing solutions.

• Capex Shortfalls: Increasing need for capital to modernize and institutionalize existing stock, as many buildings were underinvested in the last cycle.

• Demand from Value-Add Equity Strategies: Rising fundraising for CRE value-add strategies signals greater need for debt capital to support value creation business plans.

• Bank Regulatory Uncertainty: Banks are taking a cautious and highly selective approach, creating demand for alternative debt sources and flexible financing solutions.

4 Mortgage Bankers Association, Commercial and Multifamily Mortgage Debt Outstanding, March 2025.

5 PREA Quarterly, How CRE Debt Can Boost Pension Fund Portfolios, Summer 2024.

6 PGIM Real Estate, Four Compelling Reasons to Diversify with Private Real Estate Credit, June 2023.

7 PGIM Real Estate, Private Real Estate Debt: A Portfolio Risk-Return Enhance Through the Lens of Maximum Drawdowns, August 2023.

8 PREA Quarterly, Stability and Resilience in Uncertain Times: The Strategic Role of Core Real Estate Debt in Fixed Income Portfolios, Winter 2024.

Exhibit 2: Private CRE Credit Market Comparable to Major Fixed Income Markets

Exhibit 4: Credit Fundamentals Strengthen as Real Estate Property Values and Income Streams Improve

Sources: NCREIF, PGIM Real Estate. As of April 2025.

Forecasts are not guaranteed and may not be reliable indicator of future results.

5) Expanding Opportunity Set

The private CRE credit market offers broad exposure across various economic sectors offering diversification benefits across a portfolio.

However, the real estate investment universe is evolving, driven by a growing range of property types, creating an even broader range of investment opportunities with even more diverse exposures.

A notable shift toward more operational assets, including senior living, self-storage, data centers, student housing, co-living and hotels, reflects a focus on income generation. These assets require intensive asset management, opening up new avenues for financing value creation strategies.

Defining the next era of private credit: Four trends

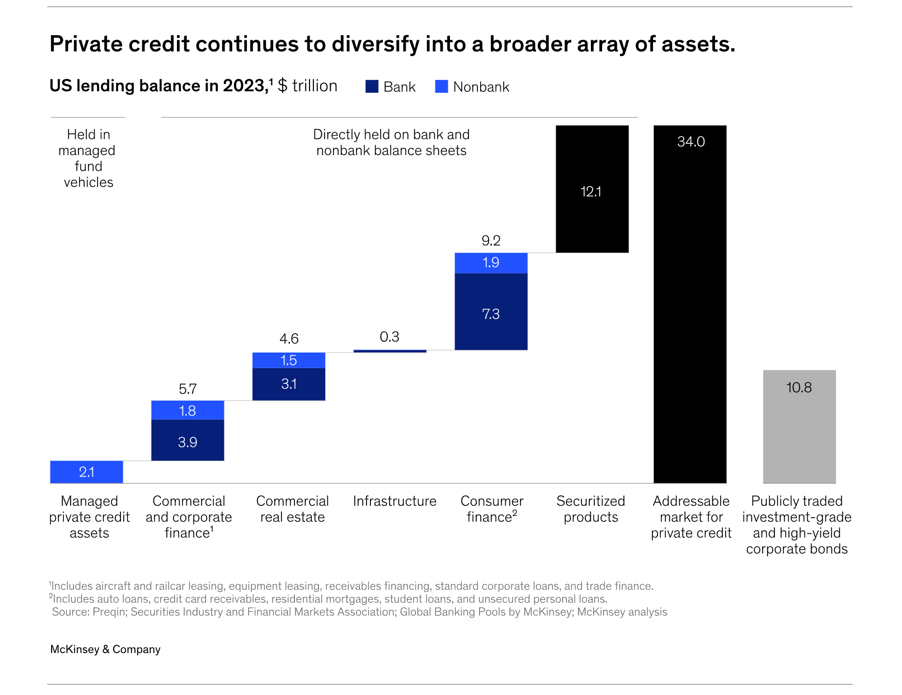

As private credit continues to grow, a new industry ecosystem with more symbiotic linkages across asset managers, banks, and insurance companies is emerging. It will support the origination, syndication, structuring, and distribution of assets at significant scale. We expect four trends to define this new ecosystem: expansion of private credit into a broader array of assets, rise of ecosystem partnerships and open-architecture business models, amplified advantages of scale for competitive differentiation, and increased focus on technology to boost scale and performance.

Expansion of private credit into a broader array of assets

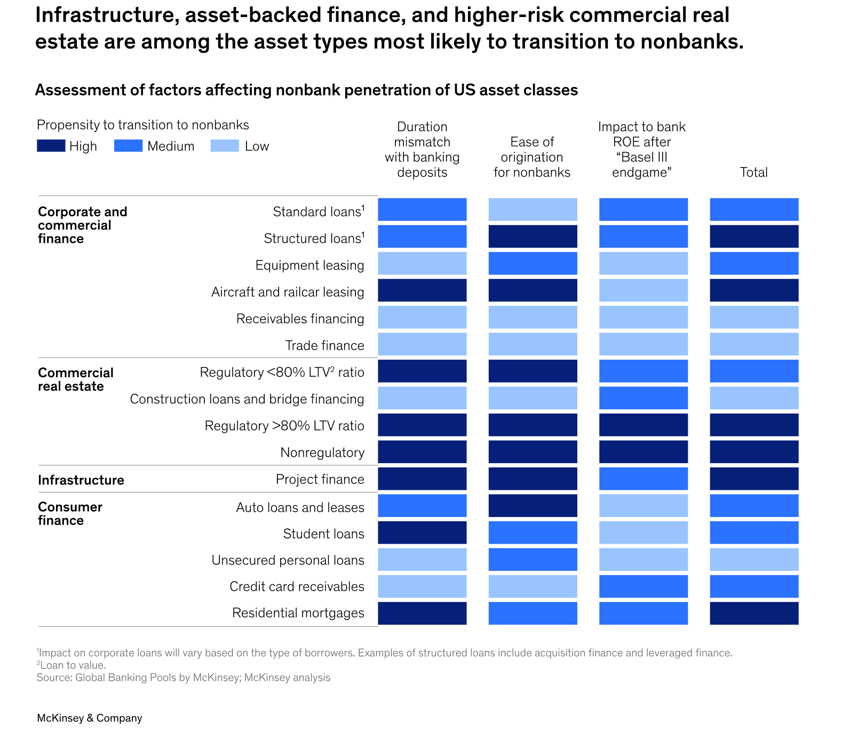

Private credit is expanding to include a broader range of asset types and new sets of borrowers. In our view, four asset classes in particular will increasingly shift to nonbank lenders:

• asset-backed finance, particularly segments that feature higher-risk-adjusted yields attractive to institutional investors (for example, aircraft loans and equipment leasing)

• infrastructure and project finance assets with relatively long durations (five years or more)

• jumbo residential mortgages, particularly those with high-loan-to-value ratios and, for non-primary residences, those that are classified as "nonconforming" under bank regulations

• higher-risk commercial real estate, for which banks are increasingly seeking to reduce their exposure

Each of these asset types ranks highly against at least one of three criteria that contribute to a propensity to transition off of bank balance sheets

Important Disclosures

For Professional and Institutional Investors only. All investments involve risk, including the possible loss of capital. Past performance and target returns are not a guarantee and may not be a reliable indicator of future results.

Links to videos and websites are intended for informational purposes only and should not be considered investment advice or recommendation to invest. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment.

PGIM Real Estate is the real estate investment management business of PGIM, the principal asset management business of Prudential Financial, Inc. (“PFI”), a company incorporated and with its principal place of business in the United States. PGIM is a trading name of PGIM, Inc. and its global subsidiaries. PGIM, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission (the “SEC”). Registration with the SEC does not imply a certain level of skill or training. PFI of the United States is not affiliated in any manner with Prudential plc, incorporated in the United Kingdom or with Prudential Assurance Company, a subsidiary of M&G plc, incorporated in the United Kingdom. Prudential, PGIM, their respective logos and the Rock symbol are service marks of PFI and its related entities, registered in many jurisdictions worldwide. In the United Kingdom, information is issued by PGIM Private Alternatives (UK) Limited with registered office: Grand Buildings, 1-3 Strand, Trafalgar Square, London, WC2N 5HR. PGIM Private Alternatives (UK) Limited is authorised and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number 181389). These materials are issued by PGIM Private Alternatives (UK) Limited to persons who are professional clients as defined under the rules of the FCA. In the European Economic Area (“EEA”), information is issued by PGIM Luxembourg S.A. with registered office: 2, boulevard de la Foire, L1528 Luxembourg. PGIM Luxembourg S.A. is authorized and regulated by the Commission de Surveillance du Sector Financier in Luxembourg (registration number A00001218) and operating on the basis of a European passport. In certain EEA countries, this information, where permitted, may be presented by either PGIM Private Alternatives (UK) Limited or PGIM Limited in reliance of provisions, exemptions, or licenses available to either PGIM Private Alternatives (UK) Limited or PGIM Limited under temporary permission arrangements following the exit of the United Kingdom from the European Union. PGIM Limited and PGIM Private Alternatives (UK) Limited have their registered offices at: Grand Buildings, 1-3 Strand, Trafalgar Square, London WC2N 5HR. PGIM Limited is authorized and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number: 193418). PGIM Private Alternatives (UK) Limited is authorized and regulated by the Financial Conduct Authority (“FCA”) of the United Kingdom (Firm Reference Number: 181389). These materials are issued by PGIM Luxembourg S.A., PGIM Limited or PGIM Private Alternatives (UK) Limited to persons who are professional clients as defined in the relevant local implementation of Directive 2014/65/EU (MiFID II) and/or to persons who are professional clients as defined under the rules of the FCA. PGIM operates in various jurisdictions worldwide and distributes materials and/or products to qualified professional investors through its registered affiliates including, but not limited to: PGIM Real Estate (Japan) Ltd. in Japan; PGIM (Hong Kong) Limited in Hong Kong; PGIM (Singapore) Pte. Ltd. in Singapore; PGIM (Australia) Pty Ltd in Australia; PGIM Luxembourg S.A., and PGIM Real Estate Germany AG in Germany. For more information, please visit pgimrealestate.com.

These materials represent the views, opinions and recommendations of the author(s) regarding the economic conditions, asset classes, securities, issuers or financial instruments referenced herein. Distribution of this information to any person other than the person to whom it was originally delivered and to such person’s advisers is unauthorized, and any reproduction of these materials, in whole or in part, or the divulgence of any of the contents hereof, without prior consent of PGIM Real Estate is prohibited. Certain information contained herein has been obtained from sources that PGIM Real Estate believes to be reliable as of the date presented; however, PGIM Real Estate cannot guarantee the accuracy of such information, assure its completeness, or warrant such information will not be changed. The information contained herein is current as of the date of issuance (or such earlier date as referenced herein) and is subject to change without notice. PGIM Real Estate has no obligation to update any or all of such information; nor do we make any express or implied warranties or representations as to the completeness or accuracy or accept responsibility for errors.

These materials are not intended as an offer or solicitation with respect to the purchase or sale of any security or other financial instrument or any investment management services and should not be used as the basis for any investment decision. Past performance is no guarantee or reliable indicator of future results. No liability whatsoever is accepted for any loss (whether direct, indirect, or consequential) that may arise from any use of the information contained in or derived from this report. PGIM Real Estate and its affiliates may make investment decisions that are inconsistent with the recommendations or views expressed herein, including for proprietary accounts of PGIM Real Estate or its affiliates.

The opinions and recommendations herein do not take into account individual client circumstances, objectives, or needs and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients or prospects. No determination has been made regarding the suitability of any securities, financial instruments or strategies for particular clients or prospects. For any securities or financial instruments mentioned herein, the recipient(s) of this report must make its own independent decisions.

Conflicts of Interest: Key research team staff may be participating voting members of certain PGIM Real Estate fund and/or product investment committees with respect to decisions made on underlying investments or transactions. In addition, research personnel may receive incentive compensation based upon the overall performance of the organization itself and certain investment funds or products. At the date of issue, PGIM Real Estate and/or affiliates may be buying, selling, or holding significant positions in real estate, including publicly traded real estate securities. PGIM Real Estate affiliates may develop and publish research that is independent of, and different than, the recommendations contained herein. PGIM Real Estate personnel other than the author(s), such as sales, marketing and trading personnel, may provide oral or written market commentary or ideas to PGIM Real Estate’s clients or prospects or proprietary investment ideas that differ from the views expressed herein. Additional information regarding actual and potential conflicts of interest is available in Part 2 of PGIM’s Form ADV.

INFORMATIONAL PURPOSES

These materials are for informational or educational purposes. In providing these materials, PGIM (i) is not acting as your fiduciary and is not giving advice in a fiduciary capacity and (ii) is not undertaking to provide impartial investment advice as PGIM will receive compensation for its investment management services. These materials do not take into account the investment objectives or financial situation of any client or prospective clients. Clients seeking information regarding their particular investment needs should contact their financial professional. The information contained herein is provided on the basis and subject to the explanations, caveats and warnings set out in this notice and elsewhere herein. Any discussion of risk management is intended to describe PGIM Real Estate’s efforts to monitor and manage risk but does not imply low risk. These materials do not purport to provide any legal, tax or accounting advice. These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation

Contacts

Dean Joseph Deonaldo

Investment Vice President

Americas Investment Research

dean.joseph.deonaldo@pgim.com

John Jacobs

Managing Director

Senior Portfolio Manager, U.S. Core Plus Debt Strategy

john.jacobs@pgim.com

Jeremy Keenan

Managing Director

Portfolio Manager, U.S. Core Plus Debt Strategy

jeremy.keenan@pgim.com

All information is deemed reliable but not guaranteed and should be independently reviewed and verified.

* Information in this message, including information regarding targeted returns and investment performance, is provided by the sponsor of the investment opportunity and is subject to change. Forward-looking statements, hypothetical information or calculations, financial estimates and targeted returns are inherently uncertain. Such information should not be used as a primary basis for an investor’s decision to invest. You should not invest unless you can sustain the risk of loss of capital, including the risk of total loss of capital.

NEWSLETTER

Subscribe for a monthly financing market update. Take advantage of our pulse on the market.

CONTACT

(305) 726-6972

info@primepartners.capital

Miami, FL 33101